08/03/13

3 min read

Since April 2010 the age at which women can first receive a state pension has been rising from 60. It is currently at 61 years and 5 months and is due to rise to 66 by 2020.

So far this change, first legislated in 1995, has had a strong effect in increasing employment among those women directly affected by the reform. It has also changed the behaviour of some of the husbands of the affected women – possibly because they are delaying their own retirement so they both retire together or perhaps to cover their wives’ lost pension income with additional earnings.

These are among the main findings of new research launched today by researchers at the Institute for Fiscal Studies. This report has been supported by the Nuffield Foundation and the IFS Retirement Saving Consortium.

The research uses data from the first two years since the female state pension age began to rise from age 60 in April 2010 to examine its impact on labour market outcomes. The findings show that, as a result of the one year increase in the female state pension age – from age 60 to 61 – that occurred between April 2010 and April 2012:

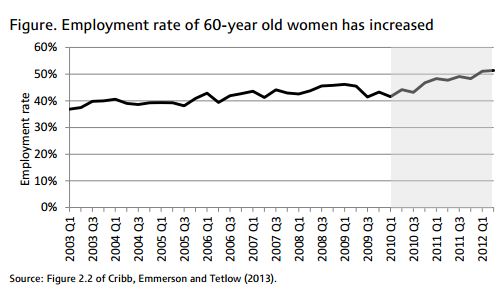

- Employment rates among 60 year old women have increased by 7.3 percentage points: in other words, in April 2012 there were 27,000 more women in work than there would otherwise have been

- Employment rates among their husbands have increased by 4.2 percentage points: in other words, there were 8,300 more men in work than there would otherwise have been

- 1.3 percentage points more women aged 60 were unemployed: in other words, there were 5,000 more women aged 60 not in work but looking for work than there would otherwise be

- The UK’s public finances have been strengthened by around £2.1 billion.

It is difficult to extrapolate these results to infer the effects of the further planned increase in pension ages for men and women. However, our results suggest future increases in the state pension age will lead to a substantial increase in employment and will strengthen the public finances.

The effects we found are especially large given that most women (and men) do not retire at their state pension age. The employment rate for 60 year old women rose from 41.5% to 51.4% between 2010Q1 and 2012Q2. These effects have also been seen in the context of a weak economy which might have made staying in, or finding, work more difficult.

What is causing this change? Increasing the state pension age does affect the financial return to remaining in paid work. However the size of the effect we find suggests that things other than these pure financial incentives are at work. In the first place women may be using the state pension age as an “anchor” in making their retirement decisions. The change in pension age could change social norms. In addition there is evidence that some women did not realise in time that their state pension age was no longer 60 and so did not take action, for example to increase saving, to offset the effect.

Jonathan Cribb, a research economist at the Institute for Fiscal Studies and a co-author of the report, said, “Increasing the age at which women can first receive their state pension has led to significant numbers of women deferring their retirement, with over half of women aged 60 now in paid work for the first time ever. We also find that some husbands are responding by remaining in work for longer. Taken together, there were 35,000 more men and women in work as a direct result of the increase in the female state pension age – from age 60 to 61 – that occurred between April 2010 and April 2012. So, despite the weak performance of the UK economy over these two years, many have been able to limit the loss of state pension income through increased earnings. These results apply only to the first groups affected and how women and men respond may change as the pension age rises further. But this is initial evidence that raising pension ages can have significant positive effects on employment.”

Notes

1.“Incentives, shocks or signals: labour supply effects of increasing the female State Pension Age in the UK” by Jonathan Cribb, Carl Emmerson and Gemma Tetlow, will be presented at 10am on Friday 8th March 2013 at the Nuffield Foundation.

2. This research is funded by the Nuffield Foundation and the IFS Retirement Saving consortium which comprises Age UK, Association of British Insurers, Department for Work and Pensions, Financial Services Authority, HM Treasury, Investment Management Association, Money Advice Service, National Association of Pension Funds, Partnership Pensions and the Pensions Corporation. Co-funding from the ESRC funded Centre for the Microeconomic Analysis of Public Policy at IFS (grant number RES-544-28-5001) is also gratefully acknowledged.

3. The Nuffield Foundation is an endowed charitable trust that aims to improve social well-being in the widest sense. It funds research and innovation in education and social policy and also works to build capacity in education, science and social science research. The Nuffield Foundation has funded this project, but the views expressed are those of the authors and not necessarily those of the Foundation.